How to Open a US Bank Account From Abroad in 2026

Living overseas but need US banking that actually stays open? This 2026 pillar guide breaks down the CIP street-address rule (31 CFR 1020.220), the ITIN route for expats without an SSN, the five real ways to get a US bank account for expats, and why a genuine Florida residential domicile beats a PO box or mail-forwarding address. Includes FATCA, FBAR, and the new IRS paperless-refund deadline.

The Your Tax Base Editorial Team helps US citizens, green-card holders, travel nurses, digital nomads, and retirees abroad establish a legitimate state residency and keep their US bank, brokerage, and benefits accounts open. The team specializes in domicile mechanics, the federal Customer Identification Program (CIP), and the residential street-address requirements that govern US banking for people living overseas.

Quick Summary

Living abroad but needing a US bank account in 2026 hinges on one rule: the federal Customer Identification Program (31 CFR 1020.220) forces banks to keep a name, birth date, identification number, and a residential or business street address on file, and PO boxes plus mail-forwarding or virtual addresses get rejected. Without a Social Security number, an ITIN (Form W-7, roughly 7 to 11 weeks) works as the tax-ID substitute. Your realistic paths: open in person on a US trip with a passport and proof of address, use non-resident-friendly institutions like SDFCU through American Citizens Abroad or Charles Schwab, lean on neobanks such as Wise or Mercury knowing they are not FDIC-insured banks, or anchor a genuine US residential domicile in a no-income-tax state like Florida. The stakes are loss-framed and growing: the IRS goes paperless for 2026 refunds and will not direct-deposit to foreign banks, Social Security is shifting to electronic-only payments, and a foreign address on file is exactly what triggers the account freezes and brokerage closures sweeping expats today.

Key Takeaways

The address is the real obstacle, not the paperwork

Opening a US account while abroad comes down to one question the bank cannot skip: where do you actually live? Documents and tax numbers are solvable; a verifiable US residential address is the part that stops most people.

Federal law requires a residential or business STREET address

The Customer Identification Program rule (31 CFR 1020.220) forces banks to collect a name, date of birth, address, and ID number before opening any account. For an individual that address must be a residential or business street address, and the rule is only a floor, so banks routinely demand a US one on top of it.

CMRA, PMB, and mail-forwarding addresses get swept out

The rule names only PO boxes as explicitly disqualified, but in practice banks screen against the USPS CMRA flag and treat virtual mailboxes, UPS Store boxes, and mail-forwarding addresses as non-residential. They clear mail, not KYC, and surfacing one in review can trigger a freeze or closure.

An ITIN is the usual SSN substitute

Non-US persons can use an IRS ITIN (applied for on Form W-7) in place of an SSN, and CIP accepts it as a valid identifying number. Plan around timing: about 7 weeks for status, 9 to 11 weeks during the Jan 15 to Apr 30 peak or from overseas, and a Certifying Acceptance Agent abroad can authenticate documents so you avoid mailing your original passport.

The viral 340,000 purged-accounts figure is not verified

The widely repeated claim that US banks quietly closed around 340,000 expat accounts in 2025 traces to a single paywalled article with no methodology and no FDIC, CFPB, FinCEN, or mainstream corroboration. The documented trend is the mechanism, not the headline number: a foreign address on file triggers KYC re-review, restriction, or closure.

Neobanks give you account numbers, not a real bank account

Wise, Revolut, Payoneer, PayPal, and Venmo issue a US routing and account number through partner banks, but most are money services businesses, not banks. Standard balances are generally not FDIC-insured (pass-through coverage is conditional), several are residency-gated or business-only, and Treasury rules bar forwarding US federal payments to a financial institution abroad.

A Florida residential domicile is the durable fix

A genuine US residential street address satisfies the CIP street-address requirement at opening and keeps the account classified as domestic over its life. Anchoring that domicile in an income-tax-free state like Florida adds a 0 percent state income tax payoff, since Florida's constitution effectively prohibits a personal income tax.

Keep existing US accounts open by not triggering the address flag

No US law requires closing an expat's account; restriction is internal risk policy keyed to the address and country of residence on file. Brokerages are hit harder than banks because SEC-registered mutual funds generally cannot be sold to people residing outside the US, so a real US address is what keeps banking, brokerage, and credit lines alive. A false or stale address risks freezes and state-tax exposure.

IRS paperless refunds and Social Security need a US bank account

Under Executive Order 14247 the IRS is phasing out paper refund checks (2026 is the first electronic-by-default season) and will not direct-deposit refunds into foreign accounts. Social Security is going fully electronic too, and in non-IDD countries a US institution or Direct Express is the only channel, making a US account the universal rail for federal money.

This article is part of our US Expat Tax Guide series. See also: Florida Residency for Expats

Read this first: This guide is educational and reflects how the rules and bank practices generally work as of 2026. It is not legal, tax, or financial advice, and it is not a guarantee that any specific bank will open or keep your account. Bank policies, IRS guidance, and the law change. Confirm the details that apply to you with the bank, the IRS, or a qualified professional before you act.

When Daniel Okafor, a software engineer from Ohio, finally settled into an apartment in Lisbon, the first thing he did was the responsible thing: he logged into his US bank and brokerage and updated his address to his new Portuguese street. Six weeks later, a letter reached him by email. His brokerage was moving his account to liquidation-only status, meaning he could sell but no longer buy. A separate notice warned that his checking account was under review because the institution no longer had a US residential address on file for him. Daniel had not done anything wrong. He had simply told the truth about where he lived, and that single field, the address on file, flipped his accounts from domestic to foreign in the bank's eyes.

Daniel's near-miss is the most common way Americans abroad quietly lose access to US banking. It is rarely a dramatic fraud case. It is a routine compliance re-review triggered by a foreign address. He kept his accounts because he was able to put a genuine US residential street address back on file, the kind a bank can verify and a state will issue a driver's license against, rather than a PO box or a mail-forwarding drop that gets flagged and swept. The address, it turns out, is the whole game.

This 2026 guide walks through how to open a US bank account from abroad, and just as importantly, how to keep the one you already have. Here is what it covers:

- Whether you can actually open a US account from overseas, split out for US citizens and green-card holders versus non-resident foreigners

- Why your address, not your passport, is the real obstacle, and which address types banks reject

- The documents you genuinely need, including how to get an ITIN from abroad and what the so-called "$3,000 bank rule" really is

- Five concrete ways to open or keep a US account, with the honest pros and cons of each

- The durable fix: a real US residential address through Florida domicile, and how mail scanning and forwarding reach you anywhere

- How to hold on to the account you have before a foreign address triggers a freeze or closure

- Tailored notes for travel nurses, digital nomads, remote workers, retirees on Social Security, naturalized citizens and green-card holders, and returning expats

- A step-by-step checklist you can work through in order

Can you open a US bank account from abroad?

Yes, you can open a US bank account from another country, but the honest answer depends entirely on who you are. If you are a US citizen or green-card holder, the law is on your side and the only real obstacle is your address. If you are a non-resident foreigner with no US ties, it is harder: you will usually need to apply in person on a US trip or route through a fintech, and most online applications will reject you outright.

Both answers trace back to one federal rule. Under the Customer Identification Program (CIP) rule, 31 CFR 1020.220, a bank must collect four things before it opens any account: your name, your date of birth, a residential or business street address, and an identification number. Nothing in that rule limits the address to the United States, and nothing in it requires a Social Security number for a foreign person. But the CIP is a floor, not a ceiling. The statute sets only minimum standards, so individual banks and brokerages layer on stricter, risk-based policies, often a hard demand for a US street address. That gap between what the law allows and what your bank actually requires is where most applications die.

US citizens and green-card holders. You are a "US person" for banking and tax purposes. You certify that status on IRS Form W-9 with a Social Security number that is issued for life and never expires no matter where you live. So three of the four CIP items take care of themselves automatically. The fourth, your address, is the whole game. Many banks insist on a US address on file and will restrict, freeze, or close an account once a foreign address surfaces in a routine review. That is compliance policy, not a legal prohibition, which is exactly why keeping a genuine US residential address is the lever that keeps your account open. It is also tied to where you owe state income tax, because the same address governs your domicile (see our guide on whether expats pay state taxes). Opening the account is rarely your problem. Keeping a verifiable US street address on it is.

Non-resident foreigners. This is the harder path, but it is not closed. The CIP rule technically lets a non-US person substitute a passport number plus country of issuance, an alien identification card, or another government document bearing a photo in place of a Social Security number, and an ITIN obtained through IRS Form W-7 is the common stand-in. The friction is institutional: most banks' online systems demand an SSN and a US address, so they cannot process you remotely. The two realistic routes are opening in person at a branch during a US trip, where staff are far more flexible and often accept a passport or ITIN, or using a fintech account that provides US account and routing numbers with its own limits. Bank of America, for instance, requires non-residents to open in person at a financial center rather than online.

Bottom line: For Americans abroad, opening an account is rarely the hard part. Holding a verifiable US street address on file is. For non-resident foreigners, plan on an in-person branch visit or a fintech workaround, not a remote online application.

Why your address is the real obstacle

Opening or keeping a US bank account rarely breaks down over your identity. It breaks down over your address. The federal Customer Identification Program (CIP) rule, 31 CFR 1020.220, forces a bank to collect four things before it opens an account: your name, date of birth, an identification number, and an address. For an individual, that address has to be a residential or business street address. Not a label on a mailbox, not a suite number at a storefront. A real street address where a human being can be located.

That one word, street, is where most Americans abroad get swept out. CIP is a floor, not a ceiling. A genuine foreign street address technically satisfies the rule, but individual banks layer stricter, risk-based policies on top, and the address you put on the account is the field their compliance systems watch hardest. Get it wrong and you do not just fail to open. You can lose an account you have held for years.

Here is why mail drops fail. FinCEN guidance is explicit: a P.O. box does not satisfy the CIP address element. The agency contrasts a rural route number, which is acceptable because it describes the area where the customer can be found, with a P.O. box, which is not (FinCEN interagency interpretive guidance on CIP). The only box-type alternative the rule even names is an APO/FPO military box, and only for someone who has no street address of their own.

Virtual mailboxes, CMRAs (commercial mail-receiving agencies), and PMBs (private mailboxes) are a step worse in practice. The rule and FinCEN guidance name only the P.O. box exclusion outright, so treating a CMRA as non-qualifying is institutional interpretation rather than black-letter text, but the logic is hard to argue with: a commercial mail drop is neither your residential nor your business street address. The USPS keeps a queryable CMRA indicator (the DPV CMRA flag, Y or N) inside the address data that banks license, so these addresses are visibly tagged. The reported pattern, which you should treat as industry practice rather than law, is that banks and fintechs increasingly reject these addresses at onboarding and close accounts when a CMRA or virtual-mailbox address surfaces during a later KYC re-review. That is the "flagged and swept" dynamic: flagged in the USPS data, then swept out in a periodic compliance pass. We unpack how CMRA addresses differ from a real residential address, and how mail handling works around it, in our guide to mail forwarding services for US expats.

Watch out: A virtual mailbox is great for receiving mail and terrible as your address of record. The same UPS Store or mail-center suite that forwards your packages can get your checking account frozen the moment a reviewer recognizes the building as a CMRA.

You have probably seen the headline that US banks "quietly purged roughly 340,000 expat accounts in 2025." Be careful with it. That figure traces to a single paywalled Medium essay with no stated methodology and no underlying data source, and no FDIC, CFPB, or FinCEN dataset, and no mainstream outlet, corroborates it. The better-sourced number for the trend is from American Banker, which reported roughly 20,000 CFPB complaints about abrupt account closures between December 2025 and May 2026 (American Banker on the closure wave), though that count is not expat-specific. The honest takeaway is not the headline number. It is the mechanism: an address that reads as a box or a mail drop is what triggers the freeze.

| Address type | Accepted for bank KYC? | Durable? | Notes |

|---|---|---|---|

| P.O. box | No | No | FinCEN states a P.O. box does not satisfy the CIP address element. Only an APO/FPO military box is named as a substitute. |

| CMRA / PMB virtual mailbox | Usually rejected | No | Carries a USPS CMRA flag (Y/N) that banks can screen. Reported practice is rejection at opening and closure on KYC re-review. |

| Friend or family address | Sometimes clears | Fragile | The rule allows a next-of-kin or contact's street address, but it is not your home, ties you to their state's tax rules, and legal and tax notices land at their door. |

| Real residential domicile address | Yes (residential class) | Yes | A genuine residential street address is exactly what the CIP rule asks for, and it can become the address on your government ID. A bank can still apply its own policy. |

The pattern across that table is simple. Every shortcut that hides "I live abroad" behind a box or a borrowed address is the thing compliance systems are built to catch. The only address type that satisfies the rule at opening and keeps satisfying it for the life of the account is a real residential one you are genuinely entitled to use. The rest of this guide is about how to get one.

The documents you actually need

Strip away the bank-by-bank noise and opening a US account comes down to four things the federal Customer Identification Program rule, 31 CFR 1020.220, forces every US bank to collect before it opens your account: your name, your date of birth, a street address, and an identification number. Translated into what you actually hand across the desk, that is four documents.

- A government photo ID. An unexpired US passport or driver's license is the cleanest. If the ID also shows your address, which a US driver's license does, it pulls double duty: it verifies your identity and your address in one credential, which is why a license is the single strongest proof of address a bank accepts. Many banks only ask for a separate address document when the ID has no physical address on it.

- An SSN or an ITIN. US citizens and green-card holders use their Social Security number. A non-US person without an SSN typically uses an ITIN. The rule technically lets a non-US person substitute a passport number plus country of issuance, an alien-ID card, or another government document bearing a photo, but most banks demand an SSN or ITIN as internal policy for tax reporting, so in practice you need one.

- Proof of a residential street address. The CIP rule wants a residential or business street address, not a PO box. Beyond a photo ID that shows it, banks commonly accept official government mail (IRS, state tax, SSA), utility bills, a lease or mortgage statement, a bank or credit-card statement, an insurance bill, or voter registration.

- A small opening deposit. Some banks, including Chase standard checking, require no minimum to complete the application; others ask for a modest opening deposit, commonly in the 25 to 100 dollar range depending on the bank and the account.

The "dated within 60 to 90 days" requirement you will hear about is bank and agency policy, not federal law. It matters most downstream: Florida's DMV (FLHSMV) specifically wants a utility, phone, bank, or credit-card statement dated within the last 60 days when you get your license.

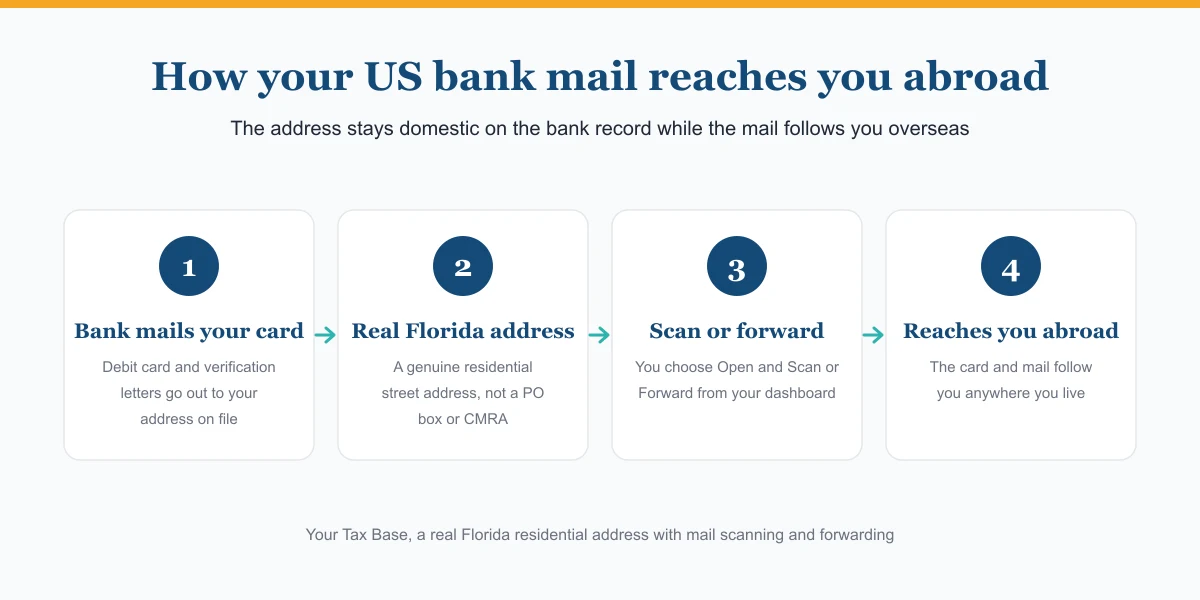

Where the address comes from: Your Tax Base gives you a genuine residential-class Florida street address that becomes the address on your bank account, and the same address on your Florida driver's license, so you hold a government ID that proves it. Mail sent there is received and then scanned to your dashboard or forwarded worldwide, which is how the debit card and verification letters reach you abroad. The Premium plan goes further with a real residential lease and a utility bill in your name, the gold-standard address proof a bank looks for. See how the residential address works.

One more piece of paper appears at opening: a tax-status form. US persons sign a Form W-9 certifying US-person status and a TIN. Nonresident aliens instead sign a Form W-8BEN certifying foreign status (and optionally claiming a treaty rate). The W-9 instructions tell foreign persons not to use it, and US persons never use a W-8.

Watch out: In 2025 regulators added an optional exemption letting a bank obtain your TIN from a reliable third-party source instead of directly from you, transmitted to banks via SR 25-2 (Federal Reserve order dated July 31, 2025). It does not eliminate any identity requirement and changes nothing you have to do: the TIN must still be obtained before the account opens.

How to get an ITIN from abroad

An ITIN is a nine-digit IRS number for federal-tax purposes, issued regardless of immigration status to people not eligible for an SSN. It does not authorize work or serve as ID outside the tax system, and you apply on Form W-7. A valid passport is the only stand-alone document that proves both identity and foreign status; otherwise you need two of 13 accepted documents, at least one with a photo.

From overseas the smart route is a Certifying Acceptance Agent. A CAA authenticates your documents on the spot and returns them immediately, so you never mail your original passport to the IRS, and CAAs operate in more than 40 countries. You can also mail Form W-7 to the IRS Austin Service Center or apply in person at a Taxpayer Assistance Center. Plan for time: the IRS notifies you of status in about 7 weeks, stretching to 9 to 11 weeks if you file during the January 15 to April 30 peak or from abroad. The IRS walks through the options in its guidance on obtaining an ITIN from abroad. A bank may even open your account while your ITIN application is pending, as long as it confirms you filed and gets the number within a reasonable time, though that is a permissive option the bank builds into its policy, not a right.

What is the $3,000 bank rule?

The "3,000 dollar bank rule" is not a tax or a reporting trigger. It is a Bank Secrecy Act recordkeeping rule, 31 CFR 1010.415. When a bank sells you a cashier's check, money order, bank draft, or traveler's check for cash of 3,000 to 10,000 dollars inclusive, it must record and verify the buyer's identity and keep that entry in a Monetary Instrument Log for five years. Nothing is filed with FinCEN or the IRS. Buying a 4,000-dollar cashier's check with cash simply means the bank asks for your ID and logs it, routine and not an accusation.

Do not confuse it with two other thresholds. The bank must actually file a Currency Transaction Report for any cash transaction over 10,000 dollars (31 CFR 1010.311), and deliberately breaking up cash to dodge either requirement, called structuring, is a separate federal crime. The 3,000-dollar rule itself just generates a record the bank keeps on its own shelf.

Five ways to open or keep a US bank account from abroad

There is no single trick. There are five practical routes, and each one trades convenience for durability. Here they are, with the honest pros and cons, so you can match the method to your situation instead of finding out the limits after you have moved your money.

1. Open in person on a US trip

If you can get to the United States, walking into a branch is still the most reliable way to open a full-service account. Online applications almost always demand a Social Security number plus a US driver's license or state ID, and they reject anyone who does not have both. In-branch staff are more flexible: they will often accept an ITIN or a passport instead, which is exactly why the trip is worth it if you lack an SSN.

Bring an unexpired passport, a secondary ID, proof of a US street address (a utility bill, lease, or recent bank statement with your name and address), your SSN or ITIN if you have one, and a small opening deposit. Chase standard checking has no minimum to complete the application. Call ahead and book an appointment, because the conversation goes faster with a banker than with a website form.

Pros: the most reliable path, a real debit card, and full access to wires, deposits, and bill pay. Cons: you have to physically be in the US, and the address you put on the account does not stop mattering once you leave. A foreign address that surfaces later can still trigger a review, which the section on keeping your account open covers in detail.

2. Banks that onboard non-residents or Americans abroad

A few institutions are explicitly built to take customers who do not live at a US address, but the details decide whether they actually help you.

Charles Schwab International is the standout for people genuinely living overseas. Eligibility is decided by your residency, not your citizenship, and it can be opened remotely. The old 25,000 dollar minimum has been removed, so there is no minimum deposit now. You will need a passport or government ID, proof of residence, an SSN or tax ID, and a Form W-8BEN if you are a non-US person. The catch is that this is the brokerage product, and it generally does not come with the fee-rebate debit card that Schwab's domestic Investor Checking offers. That checking account, with its unlimited worldwide ATM-fee rebates and no foreign-transaction fees, is designed for US residents, so it is a poor fit if your address is genuinely foreign. Schwab's international account guide lists the documents.

Chase and Bank of America will open accounts for non-citizens, but in person at a branch, not online, and both still want a US address. Chase requires a primary and a secondary ID, and for a non-US citizen without a Green Card, one of those IDs must show a US address. Bank of America requires you to open at a financial center with one primary and one secondary ID, a supporting document for a physical US address, and proof of your foreign residence, but it does accept a foreign tax ID (FTIN), so a US SSN or ITIN is not required unless you have already been issued one.

HSBC, with one caution. HSBC Expat is an offshore account held in Jersey. It can be useful, but it is not a US bank account and will not give you US account and routing numbers, so do not treat it as a way to bank inside the United States.

Pros: legitimate, named institutions that knowingly serve people abroad. Cons: the truly remote option is brokerage-first, the big banks still want a US address and an in-person visit, and "international" products are not always what they sound like.

3. Establish a real US residency and domicile

The most durable route is to stop being treated as an edge case and qualify as an ordinary US resident, with a genuine residential street address on file. This is the option the rest of this guide is built around, so the next section walks through exactly how it works. If you want to jump ahead, start with how a real US residential address works.

4. Neobanks and fintechs

Fintech apps are the easiest to open from a couch abroad, and the easiest to misunderstand. Read the limits before you rely on one.

Wise gives you US account and routing numbers, but Wise is not a bank. It is a registered money services business, and the US details are issued through a partner bank. That has two consequences worth knowing. First, standard USD balances are not FDIC-insured; pass-through FDIC coverage applies only if you opt into the Interest feature, as Wise's own FDIC disclosure explains. Second, the US details can receive only USD, and they are a shaky foundation for government money.

Watch out: The IRS will only direct-deposit a refund into a US account in the taxpayer's own name, and Treasury rules prohibit forwarding federal payments such as Social Security and tax refunds to a financial institution abroad. That makes a Wise USD balance an uncertain place to route an IRS refund or a Social Security deposit. Confirm with Wise and the paying agency before you depend on it.

Revolut is not a workaround for living abroad at all. Revolut US requires a US citizen or resident alien with a valid SSN and a US residential address, so you cannot use it to create a US account from overseas. Payoneer gives freelancers and businesses receive-only "receiving accounts" through partner banks; they are business-purpose, they reject payments from your own personal accounts, and they are not meant for friends-and-family transfers. A 29.95 dollar annual fee applies if you receive under 6,000 dollars in any twelve months.

Mercury and Relay are aimed at one specific person: the owner of a US company. Both are US fintechs, not banks, that let a non-resident founder open a USD business account online with no SSN, but the account is opened in the company's name, not yours. Mercury is the more non-resident-friendly, accepting state formation papers, an IRS EIN letter, and a passport, with a business address that can be US or international. Relay requires each owner to give a physical US personal address and bans crypto. Either way you must already hold a US-formed entity and an EIN, so this is a route for LLC owners, not individuals.

Pros: fast, remote, and genuinely useful for receiving money. Cons: several are not banks, the FDIC protection is conditional, and none of them are a clean home for federal benefits or an IRS refund.

5. Use a friend's or family member's US address

The CIP rule does leave a door open here. When you have no US street address of your own, it allows the residential street address of next of kin or another contact individual, so a relative's address can technically clear a bank's onboarding. The problem is everything that happens after onboarding.

This route is fragile for reasons that have nothing to do with opening day. The address has to stay on file for the life of the account, which means your debit card, replacement cards, and every bank letter land at someone else's house, and you are dependent on them to forward it reliably. The address is not neutral either: it can pull your tax domicile into their state, possibly a high-tax one, and legal and tax notices will arrive there too. If they move, or the relationship cools, you lose the address your accounts depend on.

Watch out: Claiming an address where you do not genuinely live is different from listing a relative as a contact. Banks cross-reference IP addresses, phone numbers, and login patterns, so foreign logins against a US "home" address can trigger a freeze, and using an address you have no real connection to carries compliance and state-tax-domicile risk. The durable fix is an address you are actually authorized to use as your home, which is the subject of the next section.

Pros: free, and it can satisfy the address field at opening. Cons: it is the least durable option on this list, it makes your mail dependent on another person, and it can create tax and compliance exposure you never signed up for.

FREE EXPAT BANKING CHECKLIST

Get the US Bank Account Setup Checklist for Expats

The step-by-step checklist for opening or keeping a US bank account while you live abroad: the CIP street-address rule, the ITIN route if you have no SSN, the documents to bring, and how a real Florida residential address keeps your account classified as domestic.

- The CIP street-address rule and which address types banks reject

- How to get an ITIN from abroad with Form W-7 and a Certifying Acceptance Agent

- The four documents to bring and the tax-status form to expect

- How a real Florida residential address keeps your account domestic

No spam. Unsubscribe anytime.

The durable solution: a real US residential address through Florida domicile

Every workaround above shares the same weak point: the address. A PO box fails the street-address test outright. A CMRA or virtual mailbox gets flagged in the USPS database and swept the next time a compliance team runs a know-your-customer review. A borrowed relative's address ties you to someone else's state, someone else's mailbox, and someone else's tax exposure. The durable fix is not a slicker mailbox. It is a genuine legal home. When you establish real Florida domicile, you stop renting an address a bank can reject and start holding one the rules were actually written to accept. That is how you stop losing access to US banking instead of patching it one onboarding screen at a time.

Here is why it clears the desk. Under the federal Customer Identification Program rule, 31 CFR 1020.220, a bank must collect and keep a residential or business street address for every account holder. Your Tax Base gives you a real residential-class Florida street address inside an actual residential community, not a PO box and not a commercial mail-receiving agency. That is the address you list on the account. And because we also help you move your license to Florida, it becomes the address printed on your Florida driver license. A government photo ID that carries your name and that exact address in one verified credential is the single strongest proof of address a bank accepts. You are not just supplying an address. You are supplying an address that a state-issued ID confirms.

The path is short, and you can start it before you fly out:

- Set up your Florida residential address. You get a genuine residential street address you can put on your bank account, driver license, voter registration, and tax return.

- File your Declaration of Domicile. We assist with the sworn statement under Florida Statute 222.17, and the signing happens through our on-platform online notary, so there is nothing to schedule and nothing to print.

- Switch your driver license and register to vote in Florida. Now your ID shows the Florida address, giving you the ID-grade proof of address banks rank highest.

- Open or update your bank account with the Florida address. As a US person you certify your status on Form W-9 using the same address, keeping the account classified as domestic rather than foreign.

- Receive the debit card and bank letters at your Florida address. Everything the bank mails lands at our processing center.

- Decide what happens to each piece from your dashboard. Hold it, Open and Scan it to read instantly, Forward it anywhere in the world, or Shred it.

That last step is what actually solves the abroad problem. A US street address is useless to you if the debit card and the verification letter sit in a box you cannot reach. When the bank mails your card or a signature-confirmation notice, you choose Forward and it follows you to your apartment overseas, or you choose Open and Scan and read the contents on your dashboard the same day, then forward the physical card when you need it in hand. The address stays domestic on the bank's records while the mail reaches you wherever you live. That is the difference between holding a US address on paper and being able to use one.

The plans, honestly: The entry tier, Essential Domicile, covers the Florida residential address, mail scanning and forwarding, and help with your license, voter registration, and Declaration of Domicile. Tax Guardian adds CPA access for your tax questions. The Premium tier goes furthest, adding a real residential lease and a utility bill in your own name, the gold-standard documents some banks ask for when they want a second proof of address beyond your ID. You can see current pricing on our pricing page.

There is one honest limit to state. A residential-class address plus a Florida driver license is what the CIP rule asks for, and it is far stronger than a CMRA, PMB, or foreign address that gets swept. But a bank can still apply its own internal policy, so this is not a guarantee that every institution will say yes to every applicant. What it does is put you on the right side of the requirement instead of the wrong side of it, with documentation that holds up over the life of the account rather than just at the opening screen.

Watch out: This works precisely because it is a real domicile, not a trick. The address has to be one you are authorized to use and genuinely treat as your permanent Florida home, which is exactly what the service is built around. Fabricating or borrowing an address you have no real connection to is what gets accounts frozen and closed.

Done right, the same Florida domicile that keeps your US bank and brokerage accounts open also drops your state income tax to zero, because Florida's constitution effectively prohibits a state income tax. One address, two wins. See exactly how the setup runs in how it works, read the expat-specific walkthrough on our Florida residency for expats page, and if you are about to relocate, lock it in first with our guide to establishing Florida domicile before you fly abroad.

Is establishing Florida domicile legitimate if you genuinely live abroad?

It is fair to ask this after all the warnings above about addresses that are "a trick." The honest answer turns on a distinction the law actually makes: the difference between residence and domicile. Residence is where you are physically staying right now. Domicile is your one permanent legal home, the place you treat as your base and intend to return to. The law lets the two sit in different places, and for a US citizen they often do. You can be physically resident in Lisbon or Dubai and legally domiciled in Florida at the same time. In fact, as a US citizen you always carry a US domicile in some state. The only real question is which state, and you are allowed to choose.

Courts have long described domicile as physical presence plus intent: you go to the place, and you intend to make it your home base. That is the exact line between a real Florida domicile and the borrowed-mailbox trick this guide keeps warning about. The trick is an address you have no genuine connection to, never visit, and use only to look domestic. A genuine domicile is the opposite: a real residential address you are authorized to use, an actual presence in Florida when you set it up, and real ties you maintain afterward, a Florida driver's license, voter registration, and a Declaration of Domicile you can sign truthfully because it states that Florida is your permanent legal home, not that you sleep there 365 nights a year.

Florida is unusually clean for this because it sets no minimum number of days you must be physically present to remain a resident. Once your domicile is genuinely established, you can travel or live abroad indefinitely and stay a Florida domiciliary, as long as you keep the ties and do not build a competing permanent home that another state can tax. We go deeper in our guides on whether changing your Florida domicile is legal and Florida residency with no physical-presence requirement.

The honest line: establishing Florida domicile is legitimate when Florida really is your chosen US home base and you build genuine ties to it. It becomes a problem when you fabricate a connection you do not have, or when you are quietly leaving a high-tax state like California or New York while keeping a home and a life there. If you are exiting a sticky state, severing those ties matters as much as building Florida ones, which we cover in how to change your state residency while living abroad. This is general education, not legal advice for your specific facts.

Do you have to go to Florida in person?

Mostly no. The Florida residential address, the Declaration of Domicile (many counties accept Remote Online Notarization under Florida Statute 117.295), your voter registration, and your mail handling are all set up remotely, from wherever you are right now. You do not fly in to start, and you do not fly in to keep it running.

There is one in-person step: the Florida driver's license. Federal REAL ID rules require an initial license to be issued in person, so you make a single trip to a Florida driver-license office, which many people fold into a visit they were already planning. That one trip does double duty, because it is also the genuine physical presence that helps anchor your domicile in the first place. After it, the license renews and the whole setup is maintained from abroad. You can begin everything else today and slot the license into your next trip stateside. See how the setup runs end to end.

Already getting "account under review" or closure letters? Do this now

If a bank or brokerage has already flagged, restricted, or threatened to close your account, the clock is running, often a 30, 60, or 90-day window, and the worst move is to ignore it. Here is the practical order of operations.

- Read the notice and call them. Ask exactly what they need to keep the account open. In most reviews triggered by a move abroad, the answer is a verifiable US residential address and updated know-your-customer details, not a decision to close you.

- Get a genuine US residential address on file fast. A real residential street address, not a PO box or commercial mailbox, is usually the specific thing the review is missing. A Florida residential address can be active quickly and becomes the address you give them.

- Hand them ID-grade proof. The strongest single document is a government photo ID that shows that address. Moving to a Florida driver's license that carries the address is what turns "an address on file" into proof a reviewer can actually verify.

- Keep at least one account reachable. Make sure your direct deposits, the IRS, Social Security, and your employer have a working US account so money keeps flowing while you sort out the rest.

Be realistic: putting a real US residential address on file can satisfy what most reviews are actually asking for, but it is not a guaranteed reversal. A bank can still close an account at its own discretion, and brokerage restrictions driven by securities law are harder to undo than a simple address flag. Acting in days rather than weeks is what protects you.

Keep the US account you already have

Opening a new account from abroad is hard. Quietly losing the one you have already is worse, and it happens to expats who do nothing wrong except update their address. No US law requires a bank or brokerage to close an American's account when they move overseas. The closures and freezes are internal risk policy, and the single trigger is almost always the same: the address and country of residence on file, not your citizenship. Swap your US street address for a foreign one in your online profile and you can flip your own account from "domestic" to "high-risk cross-border" with one form.

Banks are the milder case. Brokerages are where people get hurt, because the rule driving them is securities-distribution law, not just compliance caution. SEC-registered mutual funds generally cannot be sold to anyone residing outside the United States, including US citizens, and the offshore safe harbor that lets other securities trade abroad does not extend to open-end mutual funds. Those rules are decades old and were long ignored while firms used a US mailing address as cover. Tighter know-your-customer review now enforces them, which is exactly why a foreign-address change newly triggers a restriction that sat dormant for years. The American Citizens Abroad write-up on mutual fund restrictions for Americans overseas lays out the mechanics.

The progression is predictable: block on new purchases, then "liquidation-only" status, then a freeze or forced sale, then closure, often with a 30, 60, or 90-day window to move your assets out. ETFs usually survive because they trade like stocks rather than being "sold" by the sponsor, with the main exception being EU residents blocked by MiFID II and PRIIPs disclosure rules. Layered on top is AML and OFAC screening: a foreign jurisdiction raises your account's risk rating, and OFAC penalties are strict-liability, so firms stay risk-averse.

The names are familiar. Wells Fargo restricted some expat brokerage accounts to liquidation-only in early 2021. Morgan Stanley, Merrill Lynch, UBS, Ameriprise, and Edward Jones have all pulled back from cross-border relationships. Vanguard is retiring its legacy mutual-fund platform for retail investors by the end of 2025, and foreign-address holders who generally cannot transition to its brokerage platform may be left with withdrawals only or forced liquidation. Fidelity blocks new mutual-fund purchases for non-residents and will not open new accounts without a US address, though it generally lets accounts originally opened with a US address keep running. Schwab reserves standard Schwab.com for US residents and routes expats to its separate international platform.

Watch out: Do not "solve" this by leaving a stale US address on file while actually living abroad. That likely violates your account agreement, can trigger a freeze the moment the firm cross-references a foreign-IP login, phone, and login pattern, and can create state income-tax exposure in the state of that old address.

There is also a tax reason to keep the US account rather than retreat to foreign ones. Under FATCA, foreign financial institutions must report American account holders to the IRS or face 30% withholding, which is why many foreign banks limit or refuse US customers outright. Shifting your money offshore also shifts a personal reporting burden onto you: an FBAR if your foreign accounts ever topped 10,000 dollars in a year, and possibly Form 8938 on top. Those filings, and the way money you send home can be taxed, are covered in our remittance tax guide for expats and nomads.

The durable fix is address hygiene with substance behind it. A genuine US residential street address keeps your account classified as domestic and keeps you a "US person" in the firm's eyes. That is what a real Florida residential address provides: it is the address you list on the account, it becomes the address on your Florida driver's license (the strongest single proof of address a bank accepts), and incoming mail like a reissued debit card or a verification letter is received at the mail-processing center and then scanned to your dashboard or forwarded to you abroad. It is residential-class plus government ID, not a PO box or a commercial mail drop, which is the distinction firms screen for. No setup guarantees acceptance at every institution, but a real domicile is the version of this that holds up under review instead of collapsing the next time KYC runs.

How this plays out by situation

The address requirement lands differently depending on why you are abroad, but the common thread never changes: a stable US residential street address, not a PO box or a commercial mailbox, is both the rail that gets you paid and the documentary anchor that keeps your accounts classified as domestic. Here is what that means for the six most common situations.

Travel nurses

A large share of a travel nurse's pay arrives as housing and meal stipends, which are excludable from taxable wages only if you maintain a genuine "tax home" you travel away from. With no tax home, the assignment city becomes your tax home and those allowances become taxable wages, per IRS Publication 463. State auditors look at where your home is, where your bank statements are sent, and where your bank accounts are located, so a stable Florida residential address backs up the tax-home claim and also receives the ACH direct deposits your stipends are paid into. For the full breakdown, see our travel nurse zero-state-income-tax guide.

Digital nomads

A PO box alone fails the CIP street-address rule (31 CFR 1020.220), and a commercial mailbox is flagged in the USPS database and rejected by many banks and by the Florida DMV. A documented residential domicile, with a real street address, a driver's license, and voter registration, is the only option that satisfies bank onboarding, DMV residency proof, and a clean state-tax domicile at once. It is also the cleaner footprint if you are claiming the Foreign Earned Income Exclusion, since a maintained US "abode" can disqualify you. Our Florida residency guide for digital nomads walks through the setup.

Remote workers

If you work remotely for a US employer or US clients while living abroad, you are almost always paid by ACH direct deposit, which requires a US account and routing number that a purely foreign account cannot provide. The moment a foreign address goes on file, your bank can re-review and restrict or close the account under its own risk policy, cutting off the very rail your paycheck runs on. A genuine Florida residential address keeps the account classified as domestic and gives you a real US residential address to list on payroll, banking, and tax forms.

Retirees on Social Security

The 2026 filing season is the first "electronic by default" refund season, and the IRS does not direct-deposit refunds into foreign bank accounts, so you need a US bank account to receive them. Social Security pays abroad either by domestic direct deposit to a US institution or by International Direct Deposit to a foreign bank, but IDD only works in the roughly 180 countries on SSA's official list, leaving everyone else dependent on a US account. A real US residential address is most load-bearing here for keeping open the bank, brokerage, and IRA accounts that receive those deposits and pay your required minimum distributions, not for benefit eligibility itself. Filing and reporting duties continue from overseas; see our US expat tax filing requirements guide.

Naturalized citizens and green-card holders

Both are US persons whose identifying number is their SSN and who certify status on Form W-9, not a W-8BEN, so the friction is rarely the paperwork. It is the address: many banks require a US address and will freeze or close an account once a move abroad surfaces in review, a compliance policy rather than a uniform legal prohibition. Green-card holders carry an added stake, because a continuous absence over one year can presume abandonment of permanent-resident status under USCIS rules, so a maintained US residential address supports both your banking and your status.

Returning and relocating expats

Moving back creates a genuine chicken-and-egg problem: you need a verifiable US residential street address to open accounts, get a driver's license, or replace an SSN card, but you cannot easily establish one until you are physically present. A real residential domicile breaks the loop, because it satisfies the CIP street-address floor, is not flagged as a PO box or commercial mailbox, and supports a Florida Declaration of Domicile and the DMV's two-document address proof. Setting it up before or during the transition means your US residential address is ready the day you need to open the account.

The throughline: whatever brought you abroad, the fix is the same. Stop losing US banking access to a foreign address on file by anchoring to one genuine Florida residential address that your bank, your DMV, and the IRS all recognize.

Your step-by-step checklist

Here is the whole journey, from living abroad to a working US bank account, in the order that actually clears each obstacle. Print it, screenshot it, work it top to bottom. The early steps are the ones most guides skip, and they are exactly the ones that decide whether your account stays open a year from now.

- Decide your path first. US citizens and green-card holders are US persons: you certify on IRS Form W-9 with a Social Security number and have the widest choice of banks. Non-resident foreigners certify on Form W-8BEN and usually open in person or through a non-resident product. Knowing which lane you are in tells you which documents and which banks to chase.

- Secure a real US residential street address. The federal Customer Identification Program rule (31 CFR 1020.220) makes the bank keep a residential or business street address on file, and PO boxes, CMRA and virtual-mailbox addresses get rejected and periodically swept. A genuine residential-class address in a no-income-tax state like Florida satisfies that requirement and, once it is on your Florida driver license, gives you government-ID-grade proof of address. See how the residential address works.

- Get your SSN or ITIN sorted. US persons already have an SSN for life. Non-residents without one apply for an ITIN on Form W-7, often through a Certifying Acceptance Agent abroad so you never mail your original passport. Allow about 7 weeks for status, 9 to 11 weeks if you file from overseas or during the January 15 to April 30 peak.

- Gather ID and proof of address. An unexpired passport, a secondary photo ID, a proof-of-address document (your driver license, a utility or bank statement, or a lease), and a small opening deposit. Florida statements must be dated within the last 60 days, so time this step.

- Choose a bank or a fintech. Traditional banks and expat-friendly credit unions give you a true insured account; fintechs give you US account and routing numbers faster but with real limits. Pick the one that fits your path from step 1.

- Open the account, in person or online. Lacking an SSN, book a branch appointment on a US trip, where staff often accept a passport or ITIN that online forms reject. If you qualify online, finish it remotely.

- Set your mail to scan or forward. Point the bank's debit card and verification letters to your residential address, then from your dashboard choose Hold, Open and Scan, Forward, or Shred on each piece. This is how the card and the letters actually reach you abroad. More on the mechanics here.

- Update every direct deposit. Give the IRS your new address on Form 8822 (a change told only to a payor does not count as notice), update Social Security, and hand your employer or agency the new account and routing numbers so paychecks, refunds and benefits land in the right place.

Work the list in order and the catch-22 dissolves one step at a time: a real address unlocks the ID, the ID unlocks the account, and the account keeps your US financial life running no matter which country you wake up in.

Frequently asked questions

Can I open a US bank account from another country?

Yes. No federal law bars someone abroad from opening a US bank account. The Customer Identification Program rule (31 CFR 1020.220) only requires a bank to collect your name, date of birth, a residential or business street address, and an ID number. Most traditional banks, though, want you to apply in person on a US trip, and they set stricter policies than the law's minimum.

Can a foreigner open a US bank account online?

Rarely. Most banks' online applications are built for applicants who already have a US Social Security number and a US driver's license or state ID, so a foreigner abroad usually cannot finish them. In-branch staff are more flexible and may accept a passport or ITIN. Online fintechs like Wise can give you US account and routing numbers, but they are not banks.

Do I need a US address to open a US bank account?

Not by federal law. The CIP rule (31 CFR 1020.220) accepts any residential or business street address, including a genuine foreign one. In practice, though, many US banks demand a US street address as their own policy and keep it on file for the life of the account. A real residential Florida address, used truthfully, satisfies that requirement and reads as a US domestic account.

Can I use a virtual address or PO box for a bank account?

No. The CIP rule requires a street address, and FinCEN guidance says a PO box does not qualify. Virtual mailboxes and mail-forwarding services run through a commercial mail-receiving agency (CMRA), which USPS flags in its address database; banks can screen for that flag, and many reject or later close those accounts. You need a genuine residential-class street address, not a CMRA mail drop.

Will I lose my US bank account if I move abroad?

Not automatically. No US law forces a bank to close an expat's account. The trigger is the address and country of residence on file, not your citizenship. Once you switch to a foreign address, KYC review can freeze, restrict, or close the account, and brokerages are stricter than banks. Keeping a genuine US residential address keeps the account classified as domestic.

Can I open a US bank account without an SSN?

Yes. The CIP rule lets a non-US person use an ITIN, a passport number plus country of issuance, or another government photo ID instead of a Social Security number. Many banks still require an SSN or ITIN as internal policy for tax reporting, so an ITIN (applied for on IRS Form W-7) is the common substitute. Chase and others accept it.

Does Wise count as a US bank account?

No. Wise gives you US account and routing numbers, but Wise is not a bank; it is a registered money-services business, and the US details come through a partner bank. Standard Wise USD balances are not FDIC-insured unless you opt into its Interest feature. The numbers receive US ACH and wires, but Wise is not a substitute for a real US bank account.

What is the $3,000 bank rule?

It is a Bank Secrecy Act recordkeeping rule (31 CFR 1010.415), not a tax. When a bank sells a cashier's check, money order, or traveler's check for cash of $3,000 to $10,000, it must verify and log the buyer's identity. Nothing is filed with the IRS or FinCEN; the bank just keeps the record. Buying a $4,000 cashier's check with cash is routine, not an accusation.

How long does it take to get an ITIN?

The IRS says to allow about 7 weeks to be notified of your application status, stretching to 9 to 11 weeks if you apply during peak season (January 15 to April 30) or from overseas. The clock starts when the IRS receives your complete Form W-7 package. A Certifying Acceptance Agent can verify your passport on the spot so you avoid mailing originals.

Will the IRS deposit my tax refund into a foreign bank account?

No. The IRS does not direct-deposit refunds into foreign bank accounts. You need an open US bank account. This matters more in 2026, because Executive Order 14247 is phasing out paper refund checks, making electronic deposit the default. Without valid US banking details, a refund can be temporarily frozen, so expats benefit from keeping a US account open.

Does a Florida address help me open and keep a US bank account?

Yes, when it is a genuine residential-class street address you are authorized to use. It satisfies the CIP street-address requirement, and it becomes the address on your Florida driver's license, giving you a government photo ID that proves the address, which is the strongest proof a bank accepts. Florida also has no state income tax. A bank can still apply its own policy.

Do not lose access to US banking while you live abroad

Your Tax Base gives you a real Florida residential street address that satisfies the bank street-address requirement, puts that address on your Florida driver license as ID-grade proof, and scans or forwards every debit card and bank letter to you anywhere in the world. Establish a genuine US domicile once and keep your bank, brokerage, and federal payments flowing.

See how the US residential address works →Ready to protect your tax home?

Get IRS-compliant documentation, license tracking, and mail forwarding in one simple platform.

See Plans & PricingStay Updated on Tax Home Compliance

Get monthly tips, IRS updates, and license tracking reminders delivered to your inbox.

No spam. Unsubscribe anytime.

Related Articles

Global Expat & Migration Statistics 2026: Latest Data from the UN, World Bank, ILO & UNHCR

How many people live outside their country of birth, where they move, why they go, and what they contribute — the 2026 data reference, compiled from the latest UN DESA, IOM, ILO, UNHCR, UNESCO, World Bank, OECD and InterNations releases. Every figure is tied to a primary source and dated, with downloadable tables.

Read ArticleHow to Change U.S. State Residency While Living Abroad

Moving overseas does not end your state taxes. This 2026 playbook shows exactly how to change your U.S. state residency while living abroad: how to abandon your old domicile, establish a zero-tax state like Florida, handle the DMV and Declaration of Domicile remotely, sidestep the absentee-voting residency trap, and keep the documentation that defends you if California or New York audits you years later.

Read ArticleFlorida Domicile for Expats in 2026: How to Lock In 0% State Tax Before You Leave the US

For Americans heading abroad in 2026, the most expensive tax mistake is leaving directly from a high-tax state. Florida domicile, executed properly before you board the plane, locks in 0% state income tax, qualifies you for the federal Foreign Earned Income Exclusion at full strength, and cuts off audit risk from California, New York, and New Jersey. This is the 2026 expat playbook: a 7 to 14 day Florida residency sprint, the residential virtual address vs CMRA distinction, the calculator that shows your real savings, and a live customer case study.

Read ArticleRelated Services

Florida Residency for Expats

Maintain US ties while abroad. Florida address, mail forwarding, and tax documentation.

Learn MoreUS Expat Tax Calculator

Calculate federal taxes with FEIE ($132,900 exclusion) and Foreign Tax Credit.

Learn More